It's 11 PM and you're thinking about what happens after you're gone. Not in a morbid way, just in that practical, "I don't want to make this harder than it needs to be" kind of way.

You've worked hard. You've built something. And the last thing you want is for your family to spend the next 18 months stuck in a courtroom just to access a bank account or transfer the title on your house.

That's probate. And it's exactly what we're going to help you avoid, without hiring a lawyer, without complicated trusts, and without spending your entire weekend drowning in paperwork.

Here's the truth: probate is slow, it's public, and it's expensive. It's essentially a "final tax" on your family's time and energy during one of the hardest moments of their lives. But here's the good news, most people can sidestep a lot of it with a few simple moves you can start right now.

Let's walk through it.

Why Probate Is the Last Thing Your Family Needs

Probate is the legal process where a court oversees the distribution of your assets after you pass. Sounds official and necessary, right? In some cases, sure. But in most cases, it's just a bureaucratic speed bump that keeps your loved ones from getting what you intended them to have.

Here's what probate actually looks like:

- It's slow. The average probate process takes 6 to 18 months. Some drag on even longer if there are disputes or complications.

- It's public. Every asset you owned, every debt you owed, and every person you left something to becomes part of the public record. Anyone can look it up.

- It's expensive. Court fees, executor fees, attorney fees, they add up fast. In many states, probate costs can eat up 3% to 7% of your estate's value.

And all of this happens while your family is grieving. They're dealing with funeral arrangements, clearing out the house, and trying to hold it together emotionally. The last thing they need is a judge telling them they can't access the money in your checking account for another six months.

The good news? You can avoid most of this mess with a few simple strategies. Let's dive in.

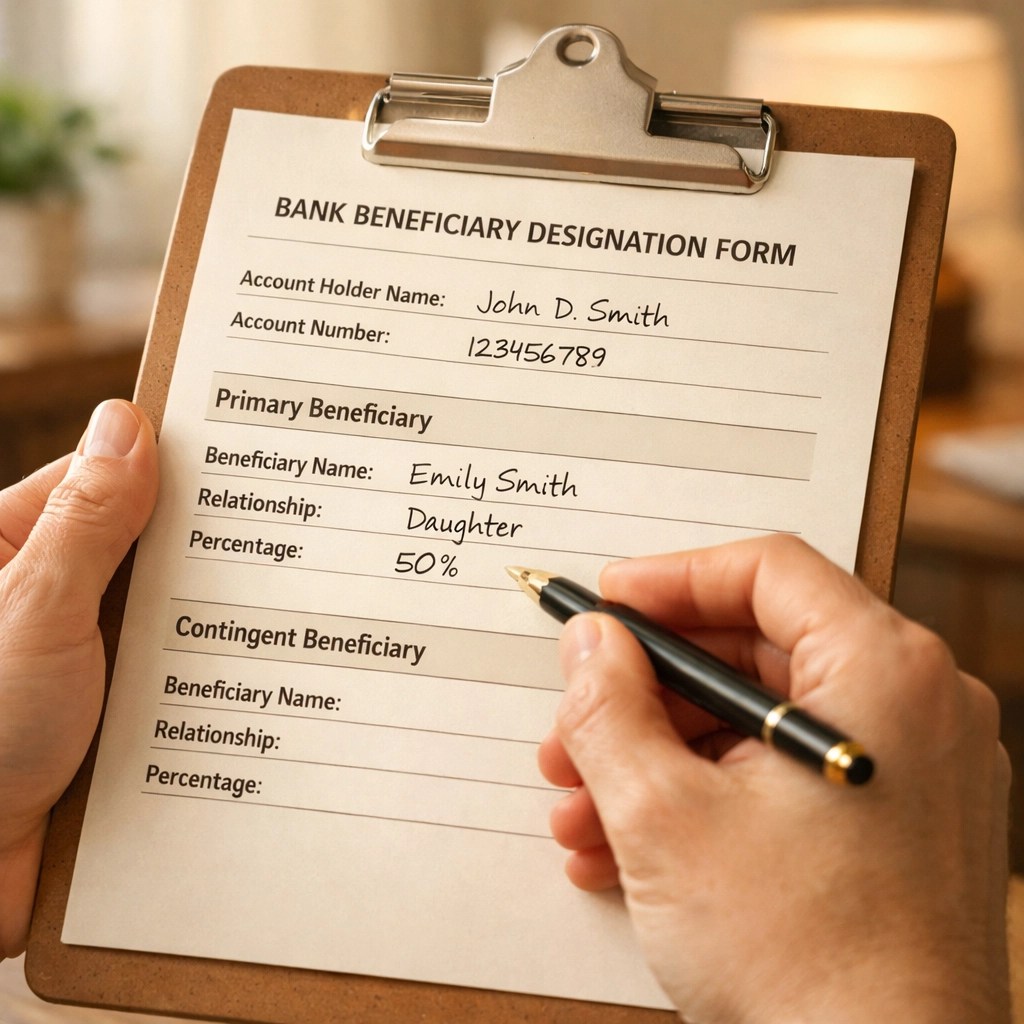

Step 1: The POD/TOD Magic Trick

Let's start with the easiest win: Payable on Death (POD) and Transfer on Death (TOD) designations.

This is one of those things that sounds too simple to be real, but it works. And it works better than a will.

Here's how it works: You contact your bank, credit union, or brokerage and tell them you want to add a beneficiary to your account. They'll give you a form. You fill in a name. Done.

When you pass away, that person walks into the bank with a death certificate, and the account transfers directly to them. No probate. No waiting. No lawyers.

POD works for:

- Checking accounts

- Savings accounts

- Certificates of deposit (CDs)

- Money market accounts

TOD works for:

- Brokerage accounts

- Stocks and bonds

- In some states, even vehicles and real estate

Most financial institutions make this process incredibly easy. You can often do it online or over the phone in less than 10 minutes per account.

Pro tip: You can name multiple beneficiaries and even set percentages. Want your three kids to split it evenly? No problem. Just make sure the math adds up to 100%.

Step 2: The Beneficiary Audit (The Low-Hanging Fruit)

Next up: the beneficiary audit. This is where most people drop the ball, and it's so easy to fix.

Life insurance policies, 401(k)s, IRAs, and other retirement accounts already have beneficiary designations built in. The problem? Most people set them up once, usually when they opened the account or started the job, and then never look at them again.

Here's what happens: Life changes. You get divorced. You remarry. A kid is born. A parent passes away. And that beneficiary form from 1998? Still sitting there with your ex-spouse's name on it.

The fix: Pull out every statement from every retirement account and life insurance policy you own. Look at the beneficiary section. Is it current? Is it who you actually want to inherit that money?

If not, call the company. Update it. It takes five minutes.

And here's the kicker: beneficiary designations override your will. So even if your will says, "Everything goes to my kids," if your 401(k) still lists your ex-husband as the beneficiary, guess who's getting that money? Your ex-husband.

Don't let this be the thing that creates drama at your funeral.

Step 3: Joint Ownership (The Pros and the Gotchas)

Joint ownership is another probate-avoidance tool, but it comes with some fine print you need to understand.

When you own property jointly with someone, whether it's a house, a car, or a bank account, it typically transfers automatically to the surviving owner when you die. No probate needed.

The most common type: Joint Tenancy with Rights of Survivorship (JTWROS). This means that when one owner passes, the other owner(s) automatically get full ownership.

This works great for:

- Your home (if you're married or have a life partner)

- Joint bank accounts with a spouse

- Vehicles titled in both names

The gotcha: Adding someone as a joint owner means they legally own that asset right now. Not when you die, now. So if you add your daughter to your house title to avoid probate, she legally owns half your house. If she gets sued, divorces, or has creditors come after her, your house could be at risk.

Joint ownership can be a useful tool, but it's not a "set it and forget it" solution. Think carefully about who you're adding and what the risks are.

Step 4: The "Letter of Instruction" Roadmap

This one isn't a legal document, but it might be the most valuable thing you do all weekend.

A Letter of Instruction is basically a roadmap for your family. It tells them where everything is, how to access it, and what your wishes are for things that don't need to be in a formal will.

Here's what to include:

- Account numbers and locations for every bank account, investment account, and insurance policy

- Usernames and passwords (or at least hints on where to find them)

- Contact information for your financial advisor, accountant, attorney, and anyone else they might need to call

- Funeral wishes (burial or cremation, what kind of service you want, etc.)

- Location of important documents (birth certificate, marriage license, property deeds, etc.)

This isn't legally binding, but it's incredibly helpful. Your family won't have to hunt through filing cabinets or guess which bank you used or whether you had life insurance.

Store it somewhere safe but accessible, like a fireproof safe at home or with a trusted family member. Make sure at least one person knows where to find it.

Step 5: When to Call a Pro (And When You Actually Need a Trust)

Here's the honest truth: not everyone needs a trust. Not everyone needs a lawyer. But some people do.

You've probably heard that a living trust is the gold standard for avoiding probate. And it's true, a trust can be a powerful tool. But it's also more complex, more expensive to set up, and requires ongoing maintenance.

You might need a trust if:

- You own real estate in multiple states

- Your estate is large enough to trigger estate taxes (in 2026, that's over $13 million for an individual)

- You have a blended family with complex inheritance wishes

- You own a business

- You want to control how and when your heirs receive their inheritance (like setting up distributions over time instead of one lump sum)

You probably don't need a trust if:

- Your estate is relatively simple (one home, some bank accounts, retirement accounts, life insurance)

- You're married and everything is jointly owned or has beneficiaries named

- You don't have complicated family dynamics or special needs dependents

If you're not sure which camp you fall into, that's where a quick conversation with a professional can save you a lot of headaches down the road.

The five steps above will get you 80% of the way there for most people. But if your situation is even a little more complicated than a basic checklist, it's worth getting a second set of eyes on it.

Take the Next Step

You've done the hard part, you've started thinking about this stuff. That's more than most people do.

But if you're sitting here thinking, "Okay, I've got the basics covered, but I'm not sure if I'm missing something," let's talk.

Schedule a quick 15-minute call with me. No pressure, no sales pitch. Just a conversation to see where you stand and whether there are any gaps we need to close. You'll walk away with clarity, and we'll figure out together if you need to do anything else.

Because here's the thing: planning ahead isn't about being morbid or pessimistic. It's about being kind. It's about making sure the people you love don't have to deal with unnecessary stress and confusion when they're already dealing with enough.

You've got this. Let's make sure your plan is as solid as the life you've built.